How the Tax-Filing Process Confuses Americans About Tax Policy

The vexed relationship people have with IRS forms tends to make them more conservative.

Most Americans don’t understand how their country’s tax system works. Even smart, educated, politically engaged people often get confused about tax policy, and the problem arises not just from what people learn from politicians or through partisan media coverage.

Over the last three years, I’ve been conducting surveys of hundreds of Americans and interviewing dozens of them, trying to capture not only what they know and think about taxes but how they arrive at those conclusions. Yes, Americans do have large and politically significant gaps in their policy knowledge. But I’ve found that those mistakes were rarely the result of a basic innumeracy or a knee-jerk opposition to taxes in general. Instead, the tax system itself draws people’s attention to certain aspects of the tax code and obscures others, making it difficult for taxpayers to accurately assess potential reforms.

Americans receive a great deal of information about taxes in their daily lives. Data about taxation is visible on receipts, pay stubs, and of course, income-tax returns. But that information is incomplete and imbalanced, and therefore misleading. Added together, the reasonable (though often wrong) conclusions people draw from this anecdotal data leave them poorly equipped to distinguish fact from fiction in debates over how the system should work.

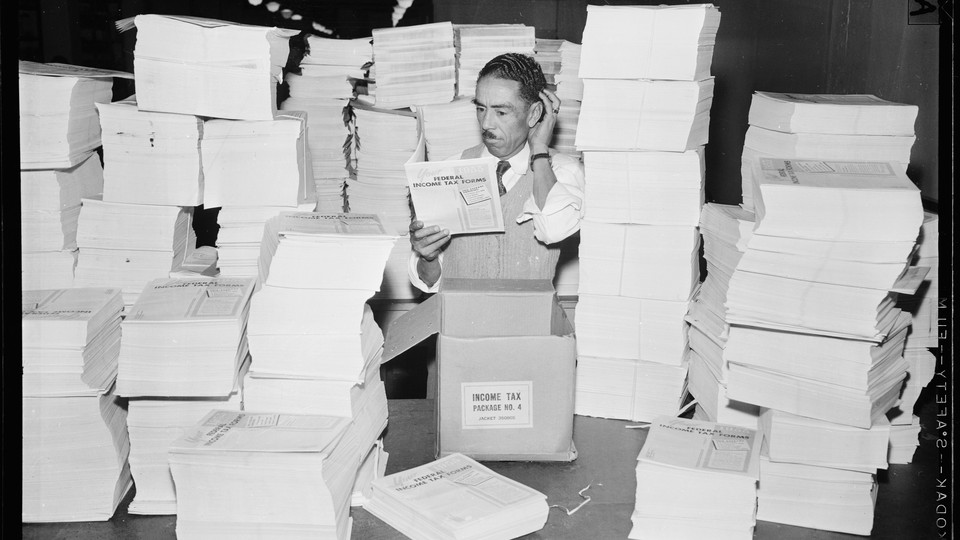

First, the inconvenient and frustrating federal income-tax filing process pushes Form 1040 to the front of taxpayers’ minds. When I asked an economically diverse national sample of 1,000 American adults which tax was most expensive for their household, most respondents—54 percent—answered the question correctly. For instance, the lowest-income respondents knew that the sales tax took the biggest bite out of their budget. But when the respondents were wrong, they almost always had picked the income tax. Interviews suggested that the filing process is such a salient memory that the income tax looms large even when its cost is (comparatively) small. As a veterinary technician in Florida told me, “It’s stressful. I feel like even after it’s done and over, I’m thinking, ‘What could I have added? What else could I have counted? What else could I have done?’”

Economists have shown that people commonly underestimate costs that are hidden from view and respond strongly to even small additional taxes that are made obvious. In this case, a focus on the income tax drives attention away from other kinds of taxes, and therefore other kinds of taxpayers. The federal income tax is a progressive tax, paid primarily by higher-income households, while sales taxes and payroll taxes eat up a bigger share of the budgets of lower-income people. When people focus on the income tax, they tend to overlook the very real expense of all the other taxes people pay. It is easy for someone in the middle class to forget the extra dollar or two they pay at the store, but for people barely making ends meet, those costs can feel onerous.

When I asked one of my lowest-income interviewees, a 53-year-old woman living on disability after an accident, about the biggest tax that she pays, she named the sales tax. “When I go to the store,” she continued, “I’m pinching pennies all the time because we never have enough food and everything.” To this woman, paying sales tax is a real sacrifice, but it’s one that people with more money often do not recognize. As one interviewee, a hairdresser from Michigan, told me, people on the “lower end” of the economic spectrum do not really count as taxpayers because “in my perception, they don’t really pay a lot.” In fact, in the U.S., the lowest 20 percent of earners pay almost 11 percent of their incomes just in state and local taxes (which include sales, income, property, and excise taxes), about twice the percentage the top 1 percent of earners end up paying in those taxes.

In addition to obscuring the taxes paid by lower-income people, the income-tax filing process draws attention toward perceived “loopholes” and away from tax rates. Income-tax filers at all income levels claim various credits and deductions, from the home-mortgage-interest deduction to the Child Tax Credit. In interviews, I found that based on their own experience of federal income-tax filing, many taxpayers assume that loopholes are the only things that matter when it comes to making the system more or less progressive.

For instance, one woman from California said she goes to “some kind of H&R Block expert,” and then complained that the wealthy can afford to hire a “hotshot accountant” to “hide” their money much more effectively than average people. A college student from California said that “the rich pay too little because of all the loopholes they have.” Very rarely did a survey respondent or interviewee mention one important policy that vastly lowers taxes for the very wealthy: historically low top tax rates.

These misunderstandings leave room for political rhetoric to steer many Americans toward tax policies different from the ones they would choose if they had better information. In 2001 and again in 2003, President George W. Bush signed legislation that cut taxes. The legislation was promoted as a great boon for middle-class families, which distracted from how heavily the tax cuts favored those with the highest incomes and also from the long-term fiscal implications of a substantial tax cut in the midst of two expensive wars.

Scholarly studies of the public response to those tax cuts present a bleak picture of the public’s capacity to assess the tradeoffs inherent in tax reform. Not long after the legislation was passed, one political scientist went so far as to compare the average taxpayer to the dimwitted cartoon character Homer Simpson, and concluded that public support for the tax cuts was due, in no small part, to “simple-minded and sometimes misguided considerations of self-interest.”

It’s important to recognize Americans’ limited policy knowledge, but accepting the limits of public information does not have to be the same as indulging in cynicism and disdain. A misunderstanding of tax policy should be viewed as an information problem, not a character flaw. The incorrect extrapolations taxpayers make based on the taxpaying process make it more likely that they’ll support tax reforms that may not benefit them.

First, confusion about who pays taxes tends to make people less likely to support government programs that help the poor. The salience of the progressive income tax leads many people to imagine that the poor pay little to no taxes, when in fact sales taxes fall on all consumers. My survey research indicates that underestimation of the taxpaying population (to which nearly every adult in the United States belongs) may help explain the strength of opposition to public spending on the poor. I found that self-identified conservative Republicans who estimate that only a third of U.S. adults qualify as “taxpayers” had a 60 percent chance of mentioning a social-safety-net program among the uses of tax dollars that upset them, whereas only 40 percent objected to welfare spending if they thought that 90 percent of U.S. adults pay taxes. In other words, conservative Republicans are far less likely to oppose welfare spending if they think of most potential beneficiaries as taxpayers. My results suggest that misleading statistics focusing exclusively on who pays federal income tax, rather than who pays any tax, can leave people less open to the social safety net than they might otherwise be.

And second, attention to loopholes, rather than tax rates themselves, encourages some people to think (wrongly) that introducing a flat tax would make higher-income people pay more in taxes. Even with all its loopholes, the United States has one of the most progressive tax systems in the world, thanks in large part to its graduated income tax. But almost a quarter of support for a flat tax comes from people who believe that such a system would actually raise taxes on the rich. A mental-health therapist I spoke to reasoned that if a flat tax did not have loopholes, the wealthy “might end up paying more even it were a lower percentage.” In reality, proposed plans to flatten the tax code would produce huge windfalls for the very wealthy. But enterprising politicians can take advantage of the public’s misperceptions: Highlight closing a few loopholes, and many Americans may miss the regressive effects of proposed rate cuts.

It is worth noting that these two misunderstandings of tax policy both tilt American preferences in one direction: to the right. Underestimating the tax responsibilities of low-income people makes it easier to oppose investment in programs to help the poor, since those Americans are seen as not paying their part. And a focus on loopholes can help obscure tax cuts for the wealthy.

Now that tax reform is back on the Congressional agenda, taxpayers are about to hear a lot about what different proposals would mean for them. There are good reasons to be concerned that many voters will be misled about the impact of the policies up for consideration. The various tax plans proposed by the Trump administration and Republican members of Congress have one major thing in common: substantial tax cuts at the very top. Those policies do not represent the preferences of most Americans. In fact, Americans’ top two concerns about taxes are that wealthy people and corporations are not paying their fair share. One might think that this frustration would shape the direction of the next round of legislation, but if and when tax-policy debates flare up in the coming months, don’t underestimate one key ingredient of tax reform: confusion borne from the taxpaying process.